How to Fill Out a W-2 Form (2026): Box-by-Box Instructions

Employers complete a W-2 for every employee paid $600 or more in a calendar year, or any amount if income tax was withheld. The form reports annual wages and all taxes withheld. Employers must distribute copies to employees by January 31 and file with the Social Security Administration (SSA) by the same date. For 2026 W-2s (reporting 2025 wages), the SSA deadline is February 1, 2026, since January 31 falls on a Saturday.

A W-2 (Wage and Tax Statement) is the IRS form employers use to report how much each employee earned and how much was withheld for federal, state, and local taxes, Social Security, and Medicare over the course of the tax year. Every employee uses their W-2 to file their personal income tax return, so accuracy matters. An error in Box 1 or an incorrect SSN can delay an employee’s refund and trigger an IRS notice.

This guide walks through every box on the form (lettered fields a through f and numbered boxes 1 through 20) with 2026 figures, plain-English explanations, and a complete Box 12 code reference.

Table of Contents

Before You Start: What You Need

Before completing a W-2, have the following information ready for each employee:

- Employee’s full legal name, current mailing address, and ZIP code

- Employee’s Social Security Number (SSN) — verify it against their Social Security card

- Your Employer Identification Number (EIN) — nine digits assigned by the IRS

- Your state employer account number (State ID), if applicable

- Year-to-date payroll data from your records: gross wages, federal/state/local withholding, FICA contributions, pre-tax benefit deductions, and deferred compensation

2026 Key Payroll Tax Figures (for 2025 wages reported on 2026 W-2s):

| Item | 2026 Figure (for 2025 tax year) |

| Social Security wage base | $184,500 |

| Social Security tax rate (employee) | 6.2% |

| Max employee Social Security tax | $11,439.00 |

| Medicare tax rate (employee) | 1.45% on all wages |

| Additional Medicare tax | 0.9% on wages over $200K (single) / $250K (MFJ) |

| Employee distribution deadline | January 31, 2026 |

| SSA filing deadline (paper & electronic) | February 1, 2026 (Jan 31 falls on Saturday) |

| E-filing required if filing | 10 or more W-2s |

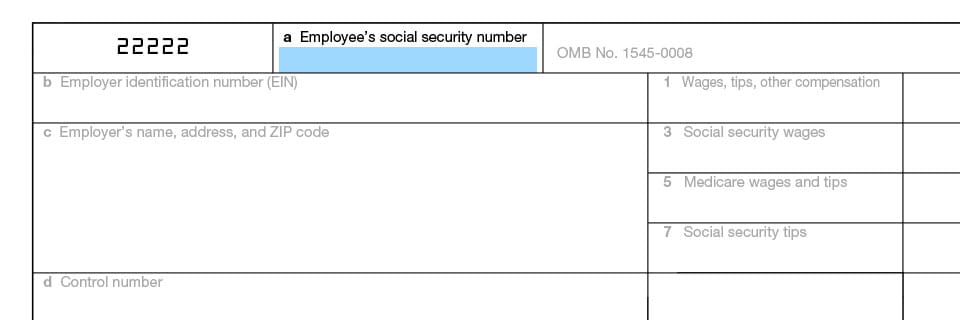

Lettered Fields (a–f): Employer and Employee Identification

The lettered fields on the left side of the W-2 establish the identity of both the employer and the employee. These fields don’t contain dollar amounts, just identifying information used by the IRS and SSA to match the form to the right people.

| Field | What to Enter |

| a | Employee’s Social Security Number (SSN). Nine digits, no dashes. Always verify against the employee’s Social Security card — a mismatched SSN is the most common W-2 error and delays SSA processing. |

| b | Employer Identification Number (EIN). Your nine-digit IRS business tax ID. Never use a Social Security Number here. |

| c | Employer’s name, address, and ZIP code. Use the exact legal business name registered with the IRS, plus the complete business mailing address. |

| d | Control number. An optional internal tracking number your payroll system may generate automatically. Leave blank if not used. |

| e | Employee’s full name. First name, middle initial, last name — exactly as it appears on their Social Security card. |

| f | Employee’s address and ZIP code. Enter the employee’s current home address. Use the most recent address on file. |

Numbered Boxes (1-20): Wages, Taxes, and Deductions

The numbered boxes run in a double column on the right-hand side and continue across the bottom of the W-2. Boxes 1–14 cover federal wage and tax information. Boxes 15–20 cover state and local tax information and appear at the bottom of the form, separated by a dotted line to allow for two sets of state/local data (useful if an employee worked in more than one state).

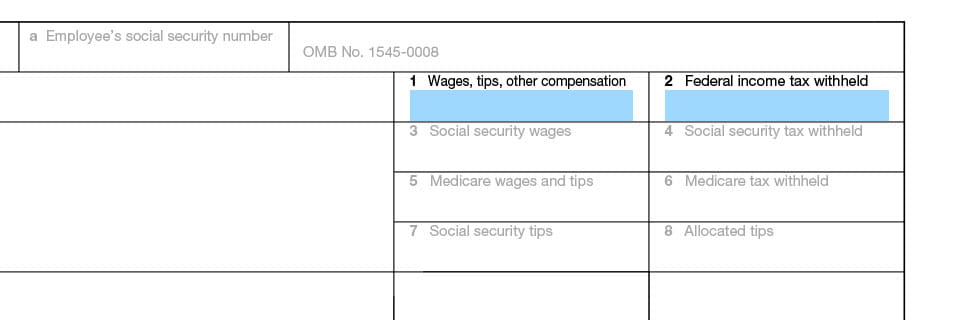

Box 1: Wages, Tips, Other Compensation

Total taxable wages for federal income tax purposes. This includes regular wages, salaries, bonuses, tips reported by the employee, and taxable fringe benefits (such as group-term life insurance premiums on coverage over $50,000). It does NOT include pre-tax benefits like 401(k) contributions, health insurance premiums under a Section 125 cafeteria plan, or HSA contributions. Those are excluded because they were deducted before tax.

Box 1 is the number employees use on their Form 1040 as their reported wages. Get this right first because everything else flows from it.

Box 2: Federal Income Tax Withheld

Total federal income tax withheld from the employee’s paychecks during the year, based on their Form W-4 elections. This is the sum of all federal income tax withholding from every paycheck across the year, not a calculation you do fresh; pull it directly from payroll records.

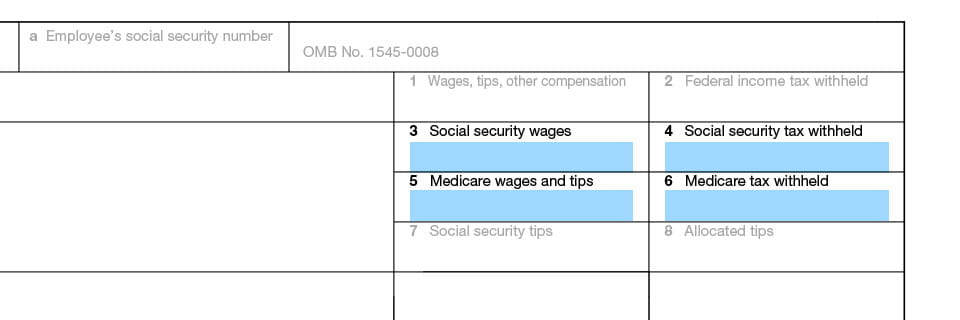

Box 3: Social Security Wages

Total wages subject to Social Security tax. For 2026 W-2s (2025 tax year): no employee should have a Box 3 figure greater than $184,500 which is the 2026 Social Security wage base. This figure does NOT include the employee’s reported tips (those go in Box 7). Pre-tax 401(k) contributions are still included here since Social Security tax is calculated before those deductions.

Box 4: Social Security Tax Withheld

The employee’s share of Social Security tax withheld: 6.2% of Box 3 wages. For 2026, the maximum amount in this box is $11,439.00 (6.2% × $184,500). If Box 4 exceeds this amount, there’s a calculation error. Employers match this amount on their own; do not enter the employer’s share here, only the employee’s.

Box 5: Medicare Wages and Tips

Total wages and tips subject to Medicare tax. Unlike Social Security, Medicare has no wage cap. Enter the full amount of taxable wages plus reported tips. This figure is typically equal to or higher than Box 3, since it isn’t capped at the Social Security wage base. Pre-tax 401(k) contributions are included here too.

Box 6: Medicare Tax Withheld

The employee’s Medicare tax withheld: 1.45% of Box 5 wages. For employees earning over $200,000 in wages (single filers) or $250,000 (married filing jointly), an additional 0.9% Medicare surtax applies. Employers must begin withholding this additional tax once they pay an employee more than $200,000 in wages in a calendar year (regardless of the employee’s filing status). The employee’s full Medicare withholding (including the surtax if applicable) goes in Box 6.

Box 7: Social Security Tips

Tips the employee reported to you during the year. When you add Box 7 to Box 3, the sum should equal Box 1 (assuming no allocated tips). Report only tips the employee actually reported — not allocated tips, which go in Box 8.

Box 8: Allocated Tips

If your business is a large food or beverage establishment (10 or more employees on a typical business day) and an employee’s reported tips fell below the IRS-approved percentage rate, you must report the difference as allocated tips here. Unlike Box 7 tips, allocated tips are NOT included in Box 1, Box 3, Box 5, or Box 7. The employee must determine whether allocated tips are taxable when they file their return.

Box 9: (Leave Blank)

Box 9 previously reported Advance Earned Income Credit payments, a program the IRS eliminated after 2010. Leave this box blank on all W-2s.

Box 10: Dependent Care Benefits

Report any amounts the employer paid or reimbursed for dependent care expenses, including contributions through a Dependent Care Flexible Spending Account (DCFSA). The first $5,000 of employer-provided dependent care benefits ($2,500 if married filing separately) is excluded from income and amounts over the exclusion limit should also appear in Box 1.

Box 11: Nonqualified Plans

Report any amounts distributed to the employee from a nonqualified deferred compensation plan or a non-governmental 457(b) plan. This amount should also appear in Box 1 as taxable wages.

Box 12: Deferred Compensation and Other Codes

Box 12 is one of the most complex parts of the W-2. You can enter up to four items in Box 12, each identified by a one- or two-letter code. Use the codes to report 401(k) contributions, HSA contributions, health coverage costs, stock option income, and about 25 other items. Up to four codes can appear on a single W-2; if an employee has more than four, you must issue a second W-2.

*The most commonly used codes are D (401(k) deferrals), W (employer HSA contributions), DD (employer health coverage cost), AA (Roth 401(k) contributions), and C (taxable life insurance over $50K).*

Complete Box 12 Code Reference:

| Code | What It Reports |

| A | Uncollected Social Security or RRTA tax on tips |

| B | Uncollected Medicare tax on tips |

| C | Taxable cost of group-term life insurance over $50,000 |

| D | Elective deferrals to a 401(k) or SIMPLE 401(k) plan |

| E | Elective deferrals to a section 403(b) plan |

| F | Elective deferrals to a section 408(k)(6) SEP |

| G | Elective deferrals and employer contributions to a section 457(b) plan |

| H | Elective deferrals to a section 501(c)(18)(D) plan |

| J | Non-taxable sick pay (not included in Boxes 1, 3, or 5) |

| K | 20% excise tax on excess golden parachute payments |

| L | Substantiated employee business expense reimbursements |

| M | Uncollected Social Security or RRTA tax on taxable cost of group-term life insurance (employees who left) |

| N | Uncollected Medicare tax on taxable cost of group-term life insurance (employees who left) |

| P | Excludable moving expense reimbursements paid directly to a member of the U.S. Armed Forces |

| Q | Nontaxable combat pay |

| R | Employer contributions to an Archer MSA |

| S | Employee salary reduction contributions to a SIMPLE retirement account (under section 408(p)) |

| T | Adoption benefits (not included in Box 1) |

| V | Income from the exercise of nonstatutory stock options (included in Boxes 1, 3, and 5) |

| W | Employer contributions to a Health Savings Account (HSA) |

| Y | Deferrals under a section 409A nonqualified deferred compensation plan |

| Z | Income under a nonqualified deferred compensation plan that fails to satisfy section 409A |

| AA | Designated Roth contributions under a section 401(k) plan |

| BB | Designated Roth contributions under a section 403(b) plan |

| DD | Cost of employer-sponsored health coverage |

| EE | Designated Roth contributions under a governmental section 457(b) plan |

| FF | Permitted benefits under a qualified small employer health reimbursement arrangement (QSEHRA) |

| GG | Income from qualified equity grants under section 83(i) |

| HH | Aggregate deferrals under section 83(i) elections as of the close of the calendar year |

Box 13: Checkboxes

Check whichever boxes apply to the employee:

- Statutory Employee: The employee is a statutory employee: meaning they work for your company but aren’t treated as a regular employee for withholding purposes (common examples: certain drivers, life insurance salespeople, home workers, and traveling salespeople). Statutory employees pay the employee share of FICA but not federal income tax via withholding.

- Retirement Plan: The employee had access to a company retirement plan (401(k), 403(b), SEP, SIMPLE, etc.) at any point during the year. Checking this may reduce the employee’s deductible IRA contribution.

- Third-Party Sick Pay: The employee received sick pay from a third party (typically an insurance company) that was included in their wages.

Box 14: Other

Use Box 14 to report any compensation or withholding not covered elsewhere on the W-2. Common uses include state disability insurance (SDI) contributions, union dues, employer-paid educational assistance, health insurance premiums for S corporation shareholders, and fringe benefits. You can use any description, just be consistent.

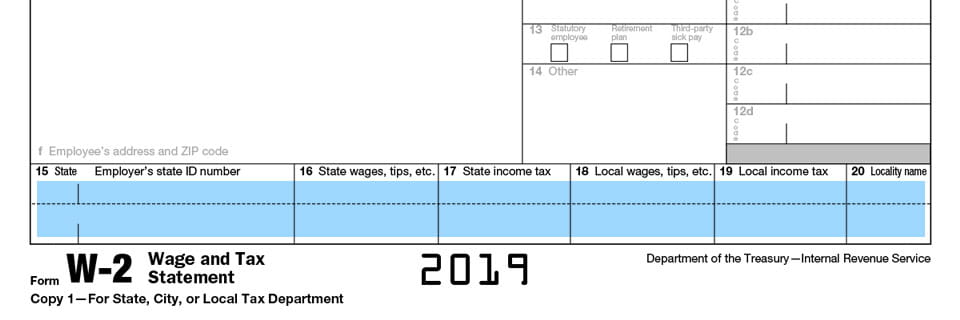

Boxes 15–20: State and Local Tax Information

These six boxes at the bottom of the W-2 handle state and local tax reporting. The bottom section is divided by a dotted line, giving you two rows which is useful when an employee worked in more than one state or locality.

| Box | What to Enter |

| 15 | State and State ID Number. Enter the two-letter state abbreviation and your state employer identification number (State ID). If you operate in a state without income tax, leave this blank. |

| 16 | State wages, tips, etc. The portion of the employee’s wages taxable by the state. May differ from Box 1 due to state-specific rules. If an employee worked in multiple states, enter each state’s wages on a separate line. |

| 17 | State income tax withheld. Total state income tax you withheld from this employee during the year. |

| 18 | Local wages, tips, etc. Wages subject to local or city income tax. May differ from Box 16. |

| 19 | Local income tax withheld. Amount withheld for local taxes (city, county, school district, etc.). |

| 20 | Locality name. Enter a brief name for the local taxing jurisdiction (e.g., ‘NYC’, ‘Philadelphia’, ‘JEDD-1’). |

Six Copies of the W-2: Where Each One Goes

| Copy | Recipient and Purpose |

| Copy A | Social Security Administration (SSA). Filed electronically through SSA’s Business Services Online (BSO) or on paper (if filing fewer than 10 W-2s). Deadline: February 1, 2026. |

| Copy B | Employee. To be filed with their federal income tax return. Distribute to employees by January 31, 2026. |

| Copy C | Employee. For their personal records. Employees should keep this for at least three years. |

| Copy D | Employer. Keep for your records for at least four years. |

| Copy 1 | State, city, or local tax department (if required by the jurisdiction). |

| Copy 2 | Employee. For filing with their state, city, or local income tax return (if required). |

Don’t Forget Form W-3

Form W-3 (Transmittal of Wage and Tax Statements) is the cover sheet that accompanies Copy A of all your W-2s when you file with the SSA. It summarizes the total wages, tips, and taxes reported across all your employees’ W-2s for the year. If you file electronically through BSO, the system generates W-3 data automatically from your W-2 submissions. If you file on paper, you must complete and submit Form W-3 along with Copy A of every W-2. Never file a W-3 without accompanying W-2s.

Common W-2 Mistakes to Avoid

1) Wrong SSN: The most common and costly error. Mismatched SSNs prevent the SSA from crediting earnings to the right worker’s record. Always verify against the employee’s Social Security card before filing.

2) Incorrect Box 1 amount: Forgetting to exclude pre-tax benefits (401(k), HSA, health premiums) or including non-taxable amounts. Box 1 ≠ gross wages.

3) Box 3 over the wage base: Box 3 cannot exceed $184,500 for 2026 W-2s. An amount above that indicates a calculation error.

4) Missing Box 12 codes: Forgetting to report 401(k) deferrals (Code D), HSA contributions (Code W), or Roth contributions (Code AA) is a very common omission… and the IRS can identify it from other filings.

5) Wrong employee address: Using an old address means the employee never receives their paper copy. Always update addresses before year-end.

6) Missing the deadline: W-2 penalties start at $60 per form for filing up to 30 days late, increase to $120 per form for filings between 31 days late and August 1, and reach $310 per form for filings after August 1 or not filed at all.

7) Filing corrections improperly: If you discover an error after filing, use Form W-2c (Corrected Wage and Tax Statement) and Form W-3c. Don’t simply reissue the original W-2.

FAQs

-

What is a W-2 form?

A W-2 (Wage and Tax Statement) is the IRS form employers use to report each employee's annual wages and all taxes withheld such as federal income tax, Social Security tax, Medicare tax, and state/local taxes. Employers issue W-2s to employees and file them with the SSA each January. Employees use their W-2 to file their personal income tax return. Any employee paid $600 or more in a calendar year, or from whom any income tax was withheld, receives a W-2.

-

When do W-2s go out in 2026?

For the 2025 tax year, employers must distribute W-2s to employees by January 31, 2026. Because January 31, 2026 falls on a Saturday, the actual deadline is February 2, 2026 for employee distribution and February 1 for SSA filing. If you miss the deadline, the IRS penalty starts at $60 per form.

-

What is the Social Security wage base for 2026?

The Social Security wage base for 2026 (applied to 2025 wages reported on 2026 W-2s) is $184,500. Only the first $184,500 of an employee's wages are subject to the 6.2% Social Security tax. The maximum employee Social Security tax for 2026 is $11,439.00. There is no wage cap for Medicare as the 1.45% Medicare tax applies to all wages.

-

What goes in Box 12 on a W-2?

Box 12 uses one- or two-letter codes to report various types of deferred compensation, benefits, and other items. The most common codes are: D (401(k) elective deferrals), W (employer contributions to an HSA), DD (employer-sponsored health coverage cost), AA (Roth 401(k) contributions), C (taxable group-term life insurance over $50K), and V (nonstatutory stock option income). See the full Box 12 code table above for all codes.

-

How do you calculate Box 1 on a W-2?

Box 1 = gross wages minus pre-tax deductions.

Start with the employee's total gross pay for the year (wages, salary, bonuses, taxable fringe benefits). Then subtract pre-tax benefits that reduce taxable income (401(k) contributions, health insurance premiums under a cafeteria plan, FSA contributions, HSA contributions, and similar items). The result is the taxable wage figure that goes in Box 1.

-

Do part-time employees or seasonal workers get a W-2?

Yes, if they earned $600 or more during the year, or if any federal income tax was withheld from their pay regardless of total earnings. The process is identical to a full-time employee; just report the actual earnings and withholdings for the period they worked.